Miami's Grove Bank & Trust runs its consumer mobile channel on a digital-banking core in the Banno-style mould, with the unusual twist that the app itself aggregates outside accounts — the bank's own product description calls out "accounts from other banks and credit unions, into a single view" — so the data model behind a single Grove login is already a fanout across multiple institutions. That matters for anyone wiring this app into a downstream system, because the first design decision is whether you want only the native Grove side of the ledger or the full aggregated view the customer sees on screen.

Where the data sits inside the app

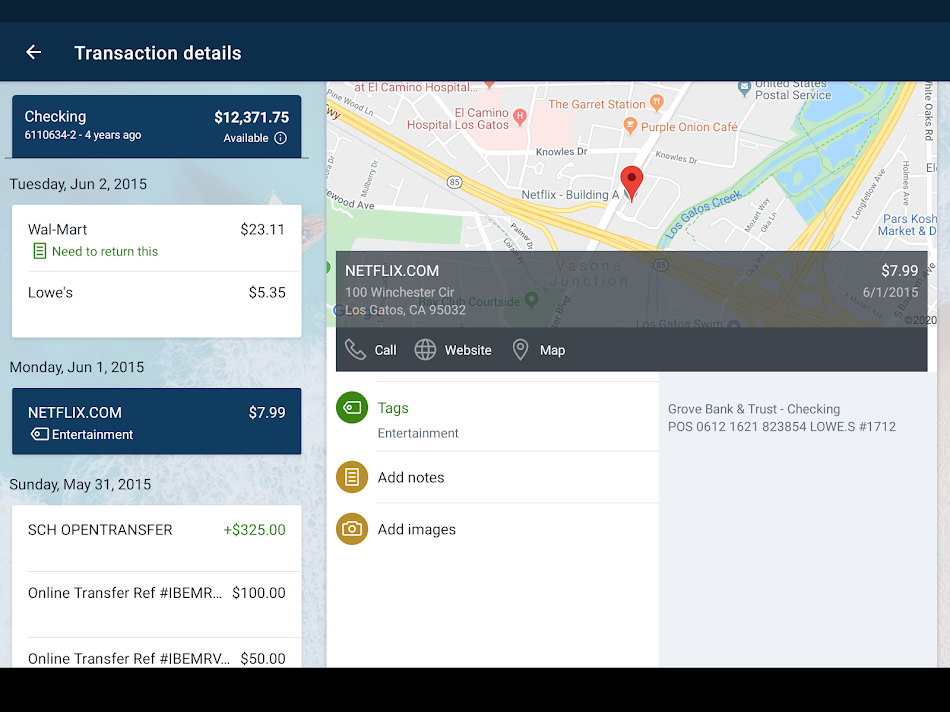

The Play Store listing and the bank's own digital-banking pages name most of the screens directly. Mapped to integration surfaces, they look like this.

| Domain | Where it lives in the app | Granularity | What an integrator does with it |

|---|---|---|---|

| Native Grove accounts | "My Accounts" header tiles | Account number (masked), balance, posted & pending transactions | Primary ledger sync — the feed your reconciliation runs against. |

| Aggregated outside accounts | Same "My Accounts" view, beneath the native tiles | Balance + transactions only; no card controls on these | Second-tier institution layer in the data model, tagged by source. |

| Transaction enrichment | Per-transaction detail screen | User-added tag strings, free-text notes, photo blobs of receipts and checks | Carry through as opaque side-channel fields — valuable for expense apps, never trimmed. |

| Mobile check deposit history | "Deposits" sub-screen | Front/back image references, amount, status (in-review / cleared / returned) | Lifecycle events into your operations queue. |

| Card controls | "My Card" panel | Card on/off state, reorder events, lost-card flag | Fraud / risk feed — rare to find on a community-bank app at this size. |

| Monthly statements | "Statements" archive | PDF per month, typically 7+ years retained | Archival pull or lender packaging. |

| Balance alerts | Notifications settings | Threshold value, channel, frequency | Replay onto your own notification rails. |

Authorized paths to that data

Three routes apply here in practice, and the right answer is almost always a combination of the first two.

1. Aggregator-mediated read on the customer's authorization

The dependable baseline. The customer authorizes a US data aggregator (Plaid, MX, or Finicity is the usual three for a US community bank of this profile) to read their Grove balances and transactions on their behalf. This is the same posture Grove itself relies on internally to fan outside accounts into its app, so the institution is already plumbed for it. Coverage is broad but plain: balances, transactions, identity, statements as offered; not card controls, not receipt photos.

2. Authorized interface integration of the mobile session

For the surfaces the aggregators don't carry — card on/off state, reorder events, receipt photo blobs, the per-transaction note strings — we run protocol analysis against the mobile session under the customer's authorization and your written scope. The mobile channel exposes these as discrete endpoints on the digital-banking core; we map the request shapes, the token-refresh chain, and the event semantics, then ship a typed client for them.

3. Native PDF/CSV statement export

Manual fallback for one-off backfills. The app exposes monthly statement downloads in its "Statements" archive; for a 24-month back-pull on a small consenting account base, this is often quicker than waiting on the live feed to catch up. Not a long-run solution — an aggregator subscription is — but it pairs well with route 1 on day one.

For most use cases we wire route 1 as the live spine and bolt route 2 on for the card and receipt surfaces a fintech actually cares about. Where the customer pool is small and audit demands strict, route 3 fills the back-history gap on first onboarding so the live feed isn't bearing that load.

What goes in the handoff

The package is biased toward code that compiles and runs against a real account on day one, with documentation behind it — not the other way around.

- Python 3.11 ingestion client covering accounts, balances, transactions, and statements, with cursor-based incremental sync and a typed result model.

- Node.js 20 webhook receiver with HMAC signature verification, exponential-backoff retry, and an idempotency table keyed on the upstream event identifier (see the snippet below).

- Automated test harness that runs the full client against a fixture account — a real consenting test customer during the build, then a sandbox identity once the engagement closes — so a future protocol shift trips the harness rather than corrupting production data silently.

- Batch-vs-realtime sync design note spelling out which domain travels on which path and how the two reconcile.

- Institution-fanout model — the data class that keeps native Grove rows distinguishable from outside-bank rows once they're in your store.

- OpenAPI 3.1 specification of the normalized surface your team consumes.

- Short auth-flow and token-refresh report covering the aggregator side and the mobile-session side.

- Compliance posture summary — how the build sits against current US consumer financial data-rights practice, and what changes if §1033 returns from reconsideration.

A working code sketch

Illustrative Node.js 20 webhook receiver, written in the shape we hand over — signed payload, replay guard, fanout to your downstream queue. Identifier names are placeholders confirmed against the aggregator account during the build.

// POST /webhooks/grove

// Bound to the consumer's authorization at the aggregator;

// fires on TRANSACTIONS_SYNC_UPDATES_AVAILABLE and INSTITUTION_ADDED.

import crypto from 'node:crypto';

import { db, queue } from './infra.js';

export async function handler(req, res) {

const sig = req.header('Aggregator-Signature') ?? '';

const expected = crypto.createHmac('sha256', process.env.WEBHOOK_SECRET)

.update(req.rawBody).digest('hex');

if (!crypto.timingSafeEqual(Buffer.from(sig), Buffer.from(expected))) {

return res.status(401).send('bad signature');

}

const evt = JSON.parse(req.rawBody.toString('utf8'));

const seen = await db.events.findById(evt.event_id);

if (seen) return res.status(200).send('replay'); // replay-safe

await db.events.put({ id: evt.event_id, ts: evt.received_at });

switch (evt.webhook_code) {

case 'TRANSACTIONS_SYNC_UPDATES_AVAILABLE':

await queue.publish('grove.tx.sync', {

item_id: evt.item_id,

cursor: evt.next_cursor,

// institution_id distinguishes native Grove rows

// from aggregated outside-bank rows in the same item.

institution_id: evt.institution_id,

});

break;

case 'INSTITUTION_ADDED':

await queue.publish('grove.institution.added', {

item_id: evt.item_id,

institution_id: evt.institution_id,

});

break;

default:

await queue.publish('grove.unhandled', evt);

}

res.status(200).send('ok');

}

The pull side is a thin Python client that takes a cursor and walks /transactions/sync until the aggregator says it's caught up; balances come on a parallel call. Worth saying out loud: the cursor is per-item, not per-institution, so a new outside account a Grove customer adds inside their app shows up as a fresh page on the same cursor, not as a separate stream.

Consent and the US data-rights status

The page reader who is going to write the consent screen needs the current US picture, not last year's. The CFPB's Personal Financial Data Rights rule (12 CFR Part 1033) was finalized in October 2024 with a phased compliance schedule for the largest data providers. On 29 October 2025 the Eastern District of Kentucky enjoined the CFPB from enforcing the rule, and the Bureau opened a reconsideration in August 2025 covering, among other things, the representative role, the fee question, and the data-security and privacy threat models — so the rule is presently not in force and the obligations as originally finalized may change before any new compliance date is set.

What that means for a Grove integration today: the dependable, settled basis is the consumer's own authorization to a US data aggregator, which is the same shape the Grove app already runs on. We design the consent surface around that — explicit scope per domain, revocation in one tap, expiry on a known window, and a logged audit trail — and we write the spec so that when §1033 (or its successor) does come into force, the call surface is a thin adapter swap rather than a redesign. Compliance posture on our side is authorized access, NDA where the customer's data model warrants it, no credential storage outside the aggregator, and minimum-necessary scope on every call.

Two things this build accounts for

The institution-fanout is real and silent. A single Grove customer's record contains a primary Grove account plus N outside accounts the customer has linked inside the app. The aggregator returns them under one item but tags each with its own institution_id. We pin that to your data model on day one, because a downstream system that flattens them ends up double-counting balances the moment a customer links a credit card from another bank. Our reference handler emits a dedicated institution_added event so new linkages flow through the same pipeline without code changes on your side.

Consent-refresh ahead of expiry. The aggregator session that backs route 1 has a finite life — somewhere around 90 days for most US aggregators — and the customer's relationship with Grove will outlast it many times over. We wire a refresh prompt into the customer-facing UX on a schedule that leaves daylight before expiry, with a fallback re-auth screen pointing to your contact at /contact.html if the prompt is dismissed. The aim is no quiet outages: the feed either runs or visibly tells the customer it needs them for a moment.

How the work is priced

For a Grove integration the typical first drop is the Python ingestion client plus the Node.js webhook receiver, wired against a single consenting account, in one to two weeks.

Source-code delivery, from $300. You take the runnable source, the tests, the OpenAPI spec, and the protocol/auth-flow notes, and you run them on your own infrastructure. Payment after delivery, once you've confirmed the build does what the brief said it would.

Pay-per-call hosted API. We host the integration and you call our endpoint. No upfront fee, no per-seat charge — metered by API call. Good when you don't want to staff the maintenance of a connector that touches a regulated data path.

Either way the engagement starts with the app name and what you need from its data; the aggregator onboarding, the test customer, and the compliance paperwork are arranged with you during the first week. Start a Grove integration

Keeping the feed honest after launch

Two reliability practices land in the handoff: a daily reconciliation job that compares aggregator-side balances against a deterministic replay of the day's webhook events and pages the on-call when they disagree by more than a configurable cent threshold, and a freshness probe that records the lag between a Grove posting and the corresponding webhook arrival. Both ship as part of the test harness, so they're enabled in CI before they ever see production.

Screens we worked against

Public Play Store screenshots, used only as visual references for the surfaces named in the data-domain table above.

How this page was put together

Drafted from the app's own Google Play listing, the bank's published digital-banking pages, the FDIC BankFind record, and the current US regulatory paperwork around §1033. Specific sources opened during the write-up:

- Grove Bank & Trust Mobile on Google Play — product description and screen list.

- FDIC BankFind — Grove Bank & Trust — charter, founding year, supervisory status.

- CFPB Personal Financial Data Rights landing page — current status of 12 CFR Part 1033.

- Personal Financial Data Rights Reconsideration — Federal Register — the August 2025 advance notice opening reconsideration.

OpenFinance Lab · ingestion engineering, 2026-05-31.

Other US apps with similar account-aggregation surfaces

Apps that an integrator would naturally compare against Grove Bank & Trust Mobile, either because they sit in the same community/regional-bank slot or because they centre on the same multi-institution aggregation feature.

- Amerant Mobile — another Florida-based community/regional bank app; similar mobile deposit and statement surfaces.

- City National Bank of Florida Mobile — Miami peer, comparable consumer mobile feature set.

- Truist Mobile — super-regional with a richer aggregation feature in-app, useful as a coverage reference.

- PNC Mobile — large-bank mobile app with native external-account linking.

- Fifth Third 53 Mobile Banking — comparable transaction enrichment and card-control surfaces.

- Bank OZK Go — regional bank app with a similar Banno-style core feel.

- Frost Bank Mobile — Texas community-bank peer, similar size class.

- Monarch Money — standalone aggregator that consumes the same kind of feed downstream of a bank like Grove.

- Copilot Money — iOS-only aggregator app, useful as a reference for what the consumer side of the data looks like in another product.

- Empower Personal Dashboard — the former Personal Capital, the most common net-worth-side consumer of US bank account feeds.

Questions integrators ask first

How fresh is the transaction feed once we wire it up?

Native Grove postings land in the feed within seconds of the bank's core posting them, because we listen on a webhook channel rather than polling on a fixed cron. Aggregated outside accounts arrive on the aggregator's own refresh interval, which is closer to a few hours; we treat the two as separate streams so the slower one doesn't drag the fast one's freshness number down.

Grove aggregates outside accounts inside its own app — do we get those too?

You can, with an explicit consent screen. The outside-bank balances and transactions visible inside Grove are themselves coming through a US aggregator on the customer's behalf, and we surface them as a second institution layer in the data model so your code can tell a native Grove debit apart from, say, a credit-card line aggregated from another issuer.

What happens when a customer adds a new external account in Grove after we've integrated?

Our reference webhook handler treats a new-institution event as a first-class signal and emits a fresh institution_added record downstream. No code change in your stack — the new account flows in through the same pipeline, tagged with its institution_id, on the next sync.

Do we need Grove to bless this before you start?

No vendor sign-off is needed to begin scoping. The dependable basis is the consumer's own authorization to read their accounts via a US data aggregator, which is how the Grove app already pulls outside accounts itself. If your use case calls for a direct relationship with the bank later, we arrange that conversation with you.

App profile (collapsed)

Name: Grove Bank & Trust Mobile

Package ID: com.grovebankandtrust.grip (per the Play Store listing)

Issuer: Grove Bank & Trust, Miami, FL — FDIC-insured commercial bank, founded 1926 per the FDIC BankFind record.

Distribution: Android (Google Play), iOS (App Store ID 1494041896).

Core features: external-account aggregation, transaction tagging with notes and receipt photos, balance alerts, person-to-person and bill payments, intra-account transfers, mobile remote deposit capture, monthly statement archive, debit-card on/off and reorder, branch and ATM locator. Login on a 4-digit passcode plus biometric on supported devices.

Enrollment: requires existing enrolment in Grove Bank & Trust online banking.

Updated 2026-05-31.